#2 High correlation and low tracking error to A-share benchmarks

Tying the index sector weights more closely to representative sectors in China’s economy can also mean closer correlation.

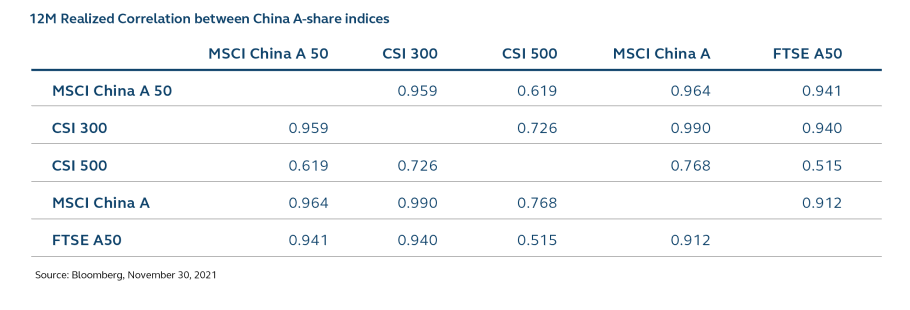

There are a range of A-share benchmarks, but the CSI 300 index - which incorporates 300 large and mid-cap stocks traded on the Shanghai and Shenzhen stock exchanges - is generally regarded as being the definitive, broad-based benchmark for A-share markets.

The MSCI China A 50 Connect Index Futures (USD) contract has demonstrated both high correlation and low tracking error to the CSI 300 benchmark index on a rolling 60-day basis since 2013, especially during volatile periods. That correlation during volatile periods - particularly during events driven by policy risk - is particularly valuable to risk managers.

#3 Appropriate sizing for institutional investors

As well as representing the complex dynamics of the A-share market, the contract has also been designed to meet the needs of what we see as an increasingly sophisticated investor base.

The market needs an institutional-sized hedging tool and the contract is four-to-five times larger than other alternatives in the offshore market.

Put together, we believe these aspects - broad-based sector composition, sizing, high correlation, low tracking error, and performance during periods of policy risk - make the MSCI China A 50 Connect Index Futures contract attractive to many different market participants.

MSCI A50: creating a richer A-share ecosystem

The MSCI China A50 Connect Index Futures (USD) Index contract also adds to the wide range of China investing products developed here in Hong Kong during the past thirty years.

The first step on that journey began with the listing of Tsingtao Brewery in 1993 and the start of the H-share market, which gave international investors access to Chinese companies.