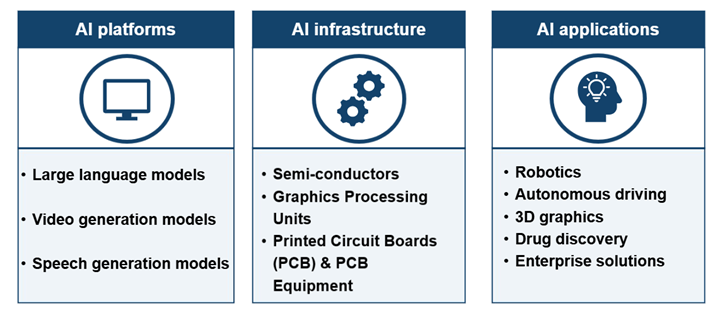

At one level are the AI platform and model companies, including MiniMax and Zhipu AI.

Around them sits an expanding applications layer: companies working in robotics, autonomous driving, 3D graphics, energy storage, drug discovery, and enterprise solutions, including names such as CiDi, OneRobotics, Insilico Medicine, Sigenergy and Manycore Technology.

Beneath that is the infrastructure layer: the chips, semiconductors, sensors, hardware that allow AI workloads to run in practice, represented by companies such as Biren Technology, Axera Semiconductor, Gpixel and Victory Giant Technology.

Taken together, these layers tell a more interesting story than any single deal could on its own.

One or two high-profile listings can create excitement, but a succession of companies spanning platforms, applications, semiconductors, image sensors, robotics, AI software and energy-linked technologies begins to create something more durable: sector depth and a stronger sense that investors can access an investable theme rather than a handful of disconnected names.

That breadth is also increasingly visible at the benchmark level, with indices such as the HKEX Tech 100 Index tracking 100 of the largest Hong Kong-listed companies across six innovation themes, including AI.

That is one of the reasons the recent IPO wave feels transformational. It suggests that AI is starting to appear in Hong Kong not only as a market narrative, but as a listed category with breadth.