Why launch the HKD-RMB Dual Counter Model now?

The RMB internationalisation process means the RMB is increasingly being used as a trading and investment currency and offshore RMB liquidity pools are growing.

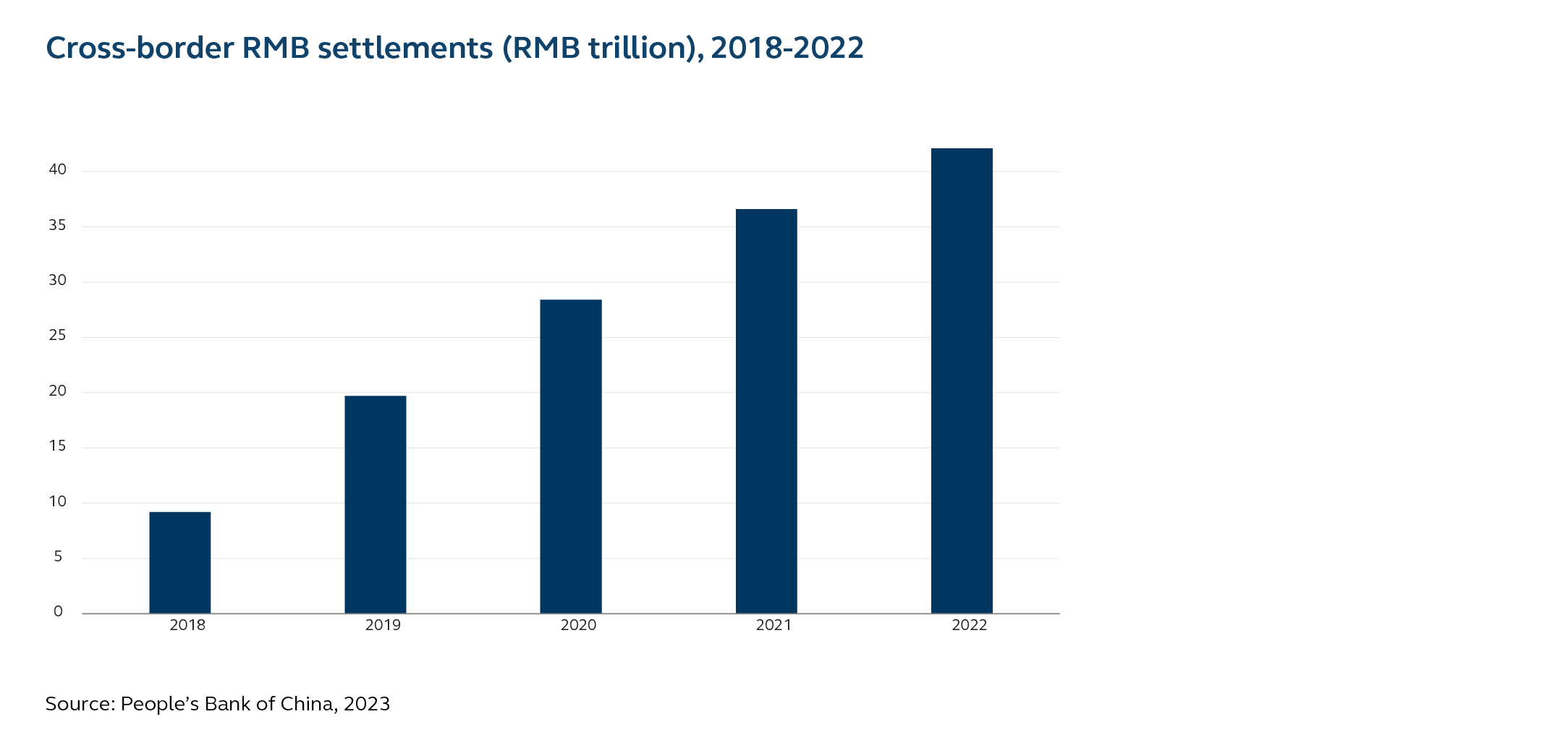

For example, RMB 42.1 trillion (USD 6.1 trillion) of China’s cross-border payments and receipts were settled in RMB during 2022, up 15% compared with RMB 36.6 trillion in 2021, and up 48.2% compared with RMB 28.4 trillion in 2020, according to data from the People’s Bank of China.

The RMB is now one of the five most actively traded currencies in the world. It rose to fifth place in over-the-counter (OTC) foreign exchange markets in April 2022, up from eighth in the same month in 2019, according to an October 2022 survey of central banks by the Bank for International Settlements (BIS).

By enriching the RMB product ecosystem with the addition of RMB-denominated securities in the Dual Counter Model, HKEX is channeling the growing vitality in the RMB space into financial markets and promoting RMB internationalisation.

Hong Kong is the world’s leading offshore RMB centre – total RMB deposits in Hong Kong have increased from RMB 597 billion in April 2018 to RMB 832 billion in April 2023, and Hong Kong was the world's largest offshore RMB settlement center in 2020, handling approximately 75% of all global RMB payment transactions, according to the Society for Worldwide Interbank Financial Telecommunication (SWIFT).

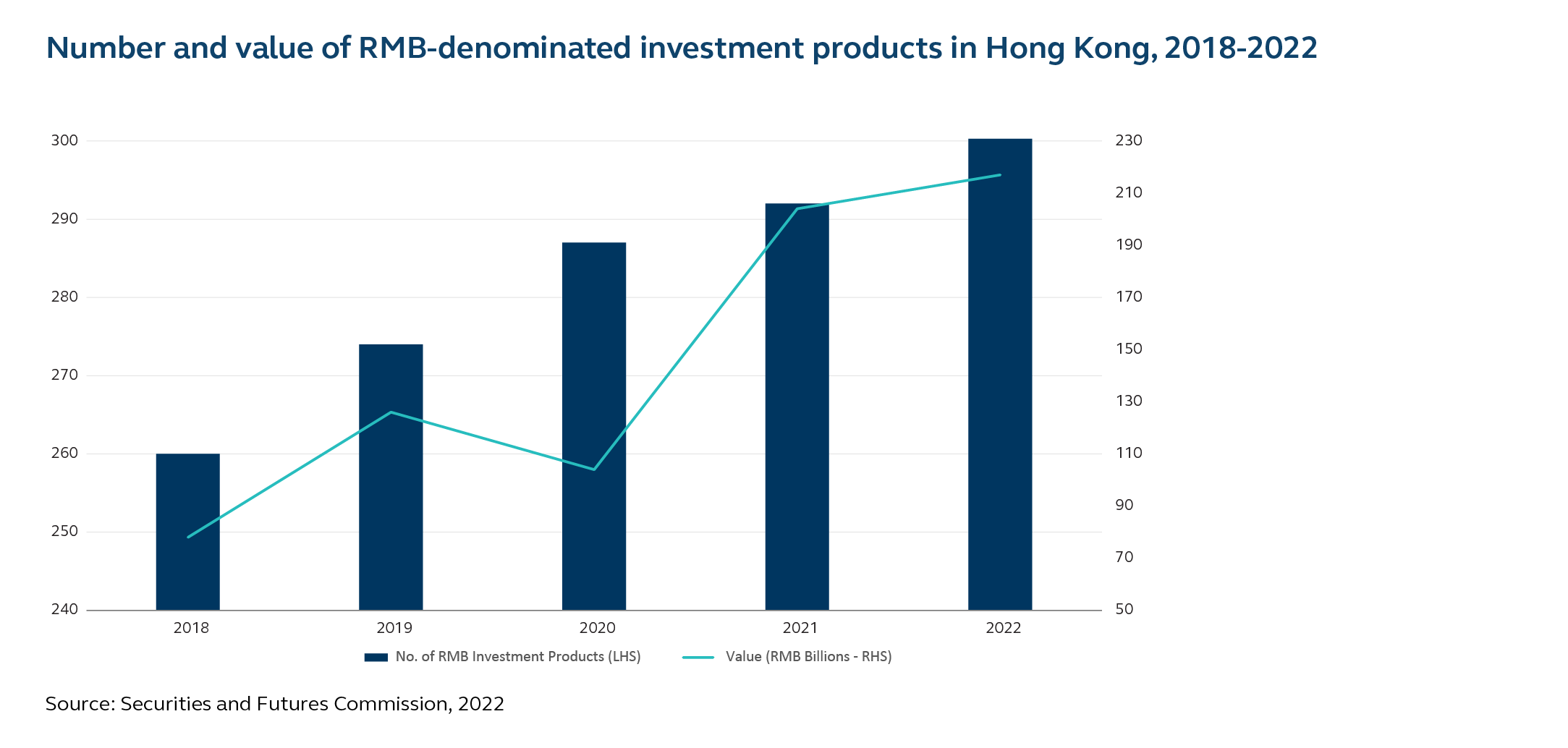

Also, the number and value of RMB-denominated investment products in Hong Kong is expanding – rising from 260 in 2018 to 342 at the end of 2022, and with the total value growing from RMB 78 billion to RMB 217 billion over the same time horizon, according to the Securities and Futures Commission.